Competition for Attention in the ETF Space

Itzhak Ben-David (The Ohio State University and NBER), Francesco Franzoni (Università della Svizzera italiana (USI)), Byungwook Kim (The Ohio State University), and Rabih Moussawi (Villanova University)

Investors appear to trust less and less the skills of active mutual fund managers and increasingly redirect their money to index-tracking products such as exchange-traded funds (ETFs). As a result, ETFs’ assets under management (AUM) have grown exponentially, starting from about zero in the early 1990s. They have surpassed $10 trillion globally, about $6.8 trillion in the U.S. only. In the U.S. alone, more than 1,000 different ETFs invest in the U.S. stock market, which consists of less than 6,000 publicly traded stocks. After observing this dramatic growth of this sector, commentators have talked about the passive revolution, industry sponsors call this trend “democratization of investments,” and policymakers work on ways to facilitate and speed up the introduction of new ETFs to the market.

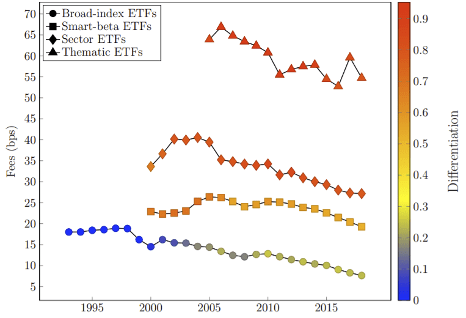

But what drives the growth in the ETFs market? Why are there are so many funds tracking combinations of stocks in which investors could invest directly? As the competition among ETFs compresses the fees that they charge, it appears that new and more expensive products are introduced. Over time, ETFs become more specialized, i.e., investing in sectors and themes that are relatively narrow. Figure 1 shows fees charged by existing ETFs and new types of ETFs being introduced.

Figure 1. The Evolution of the ETF Species (Source: Ben-David, Franzoni, Kim, and Moussawi, 2022, Review of Financial Studies, forthcoming.)

An interesting observation is that specialized ETFs tend to focus on trendy themes, i.e., sector and thematic ETFs. For example, in 2019, the newly-launched ETFs included products focusing on cannabis, cybersecurity, and video games. In 2020, new ETFs covered companies somehow related to the Black Lives Matter movement, COVID-19 vaccine, and the work-from-home trend. In 2021, among others, we had ETFs tracking Bitcoin, impact investing, and the metaverse. Typically, these specialized portfolios contain fewer securities than those in the most famous stock indexes, such as the S&P 500. Therefore, investors who choose these specialized products should be aware of the low degree of portfolio diversification.

In our project, we study the performance of specialized ETFs and compared it to the behavior of broad-based ETFs, which track well-diversified indexes. Moreover, we highlight the motives for ETF sponsors to create new products that chase popular investment themes. Focusing on the U.S. market between 2000 and 2019, we find that specialized ETFs start to deliver disappointing returns as soon as they are launched. Over the five years after their inception, on average, specialized ETFs earn an average return of about 30% lower than that of broad-based products.

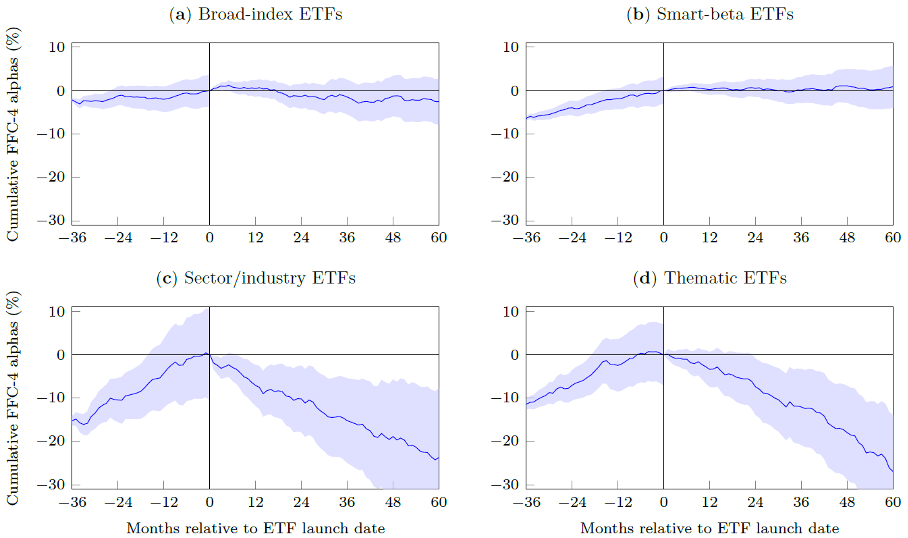

We explore different explanations for this underperformance and whether investors anticipated it at the time of inception. Among the various hypotheses, the overvaluation hypothesis is the only one that is supported by the data. According to this hypothesis, specialized ETFs are launched to cater to over-optimistic investors by offering investment products that invest in “hot” sectors and themes. However, by the time the ETF issuers identify the “hot” industry or theme, this market segment has already reached peak valuation. Hence, the specialized ETFs underperform because the securities in their portfolios are already overvalued at launch. Figure 2 shows these results. It plots the indexes in which the different types of ETFs invest, pre-launch and post-launch.

Figure 2. The indexes underlying the different types of ETFs. (Source: Ben-David, Franzoni, Kim, and Moussawi, 2022, Review of Financial Studies, forthcoming.)

Further corroborating our conjecture that specialized ETFs invest in overvalued assets is the fact that these ETFs invest in stocks that stoke investor optimism. We find that firms whose stocks are included in the portfolios of specialized ETFs receive more positive media exposure than other stocks in the time leading up to the ETF launch. Then, over time, the valuation of these firms deflates, and the specialized ETF tracking these stocks provides disappointing returns to its investors.

We also find that specialized products are trendy among Robinhood retail investors and lure typically less sophisticated retail investors. For example, large institutional investors (e.g., mutual funds, pension funds, banks, and endowments) prefer broad-based ETFs.

Chasing “hot” and overvalued investment themes appears to result from a deliberate marketing strategy pursued by ETF sponsors. Our research indicates that ETF providers operate in a tough competitive environment. Over time the margins generated by the industry have become thinner. Launching products that chase trendy investment themes allows ETF sponsors to attract investors’ attention and, at the same time, to charge higher fees. The annual expense fees that specialized ETFs charge are on average 30% higher than those of broad-based products.

To conclude, investors should be wary when approaching specialized ETFs. Our research shows that investors risk losing along three dimensions: they lose portfolio diversification, obtain disappointing performance, and pay higher fees. As a result, investors should pay special attention when considering these funds.

Authors’ Note

Our paper is forthcoming at the Review of Financial Studies. For reference, please cite:

Ben-David, Itzhak, Francesco Franzoni, Byungwook Kim, and Rabih Moussawi, 2022, Competition for Attention in the ETF Space, Review of Financial Studies, forthcoming.

A working paper version is available on https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3765063

About the Authors

Professor Itzhak (“Zahi”) Ben-David is the Neil Klatskin Chair in Finance and Real Estate at The Ohio State University Fisher College of Business. In addition, he is the Academic Director of the Ohio State University Center for Real Estate and a Research Associate at the National Bureau of Economic Research (NBER). Ben-David works in several research areas in finance, including real estate, financial intermediation, financial markets, behavioral finance, and household finance. Ben-David holds a Ph.D. in Finance and an MBA from the University of Chicago, a B.S. and an M.S. in Industrial Engineering, a B.A. in Accounting from Tel-Aviv University, and an M.S. in Finance from London Business School. Read more at https://u.osu.edu/ben-david.1/.

Professor Itzhak (“Zahi”) Ben-David is the Neil Klatskin Chair in Finance and Real Estate at The Ohio State University Fisher College of Business. In addition, he is the Academic Director of the Ohio State University Center for Real Estate and a Research Associate at the National Bureau of Economic Research (NBER). Ben-David works in several research areas in finance, including real estate, financial intermediation, financial markets, behavioral finance, and household finance. Ben-David holds a Ph.D. in Finance and an MBA from the University of Chicago, a B.S. and an M.S. in Industrial Engineering, a B.A. in Accounting from Tel-Aviv University, and an M.S. in Finance from London Business School. Read more at https://u.osu.edu/ben-david.1/.

Francesco Franzoni is Professor of Finance at the Università della Svizzera italiana (USI) in Lugano, holds a Senior Chair with the Swiss Finance Institute (SFI), and is a research fellow at the Center for Economic Policy Research (CEPR). His research concentrates on institutional investors, such as hedge funds and ETFs, and their impact on asset prices. He obtained his Ph.D. in Economics from MIT and his B.A. and M.S. in economics from Bocconi University. Read more at https://people.lu.usi.ch/franzonf/.

Francesco Franzoni is Professor of Finance at the Università della Svizzera italiana (USI) in Lugano, holds a Senior Chair with the Swiss Finance Institute (SFI), and is a research fellow at the Center for Economic Policy Research (CEPR). His research concentrates on institutional investors, such as hedge funds and ETFs, and their impact on asset prices. He obtained his Ph.D. in Economics from MIT and his B.A. and M.S. in economics from Bocconi University. Read more at https://people.lu.usi.ch/franzonf/.

Byungwook Kim is a fourth-year Ph.D. candidate in finance at The Ohio State University’s Fisher College of Business. His research interests include asset pricing, investor behavior, and asset management (ETFs, mutual funds, hedge funds). He earned a BBA from Yonsei University, and an M.S. in Statistics from the University of Chicago. Read more at https://byungwookkim.com/.

Byungwook Kim is a fourth-year Ph.D. candidate in finance at The Ohio State University’s Fisher College of Business. His research interests include asset pricing, investor behavior, and asset management (ETFs, mutual funds, hedge funds). He earned a BBA from Yonsei University, and an M.S. in Statistics from the University of Chicago. Read more at https://byungwookkim.com/.

Rabih Moussawi is an Associate Professor of Finance at Villanova University. His research interests are institutional investors, ETFs, hedge funds, and corporate governance. Before joining Villanova, Moussawi was a research director at WRDS of the Wharton School, was previously a quantitative researcher at Barclays Global Investors (now BlackRock), and taught finance at the University of Texas at Dallas. Moussawi received his Ph.D. from the University of Texas at Dallas, and his MBA and B.A. in Economics, with distinction, from the American University of Beirut. Read more at https://www.rabihmoussawi.com/.

Rabih Moussawi is an Associate Professor of Finance at Villanova University. His research interests are institutional investors, ETFs, hedge funds, and corporate governance. Before joining Villanova, Moussawi was a research director at WRDS of the Wharton School, was previously a quantitative researcher at Barclays Global Investors (now BlackRock), and taught finance at the University of Texas at Dallas. Moussawi received his Ph.D. from the University of Texas at Dallas, and his MBA and B.A. in Economics, with distinction, from the American University of Beirut. Read more at https://www.rabihmoussawi.com/.